Pensions often seem like something to think about another day. Retirement seems so far away for so many of us, but in reality, a solid pension plan is the cornerstone of a long and healthy retirement.

We're thrilled to announce the creation of the Open Finance Developers Group (OFDG), a meet-up group aimed at fostering innovation, communication and connection in the Open Finance and Open Banking communities.

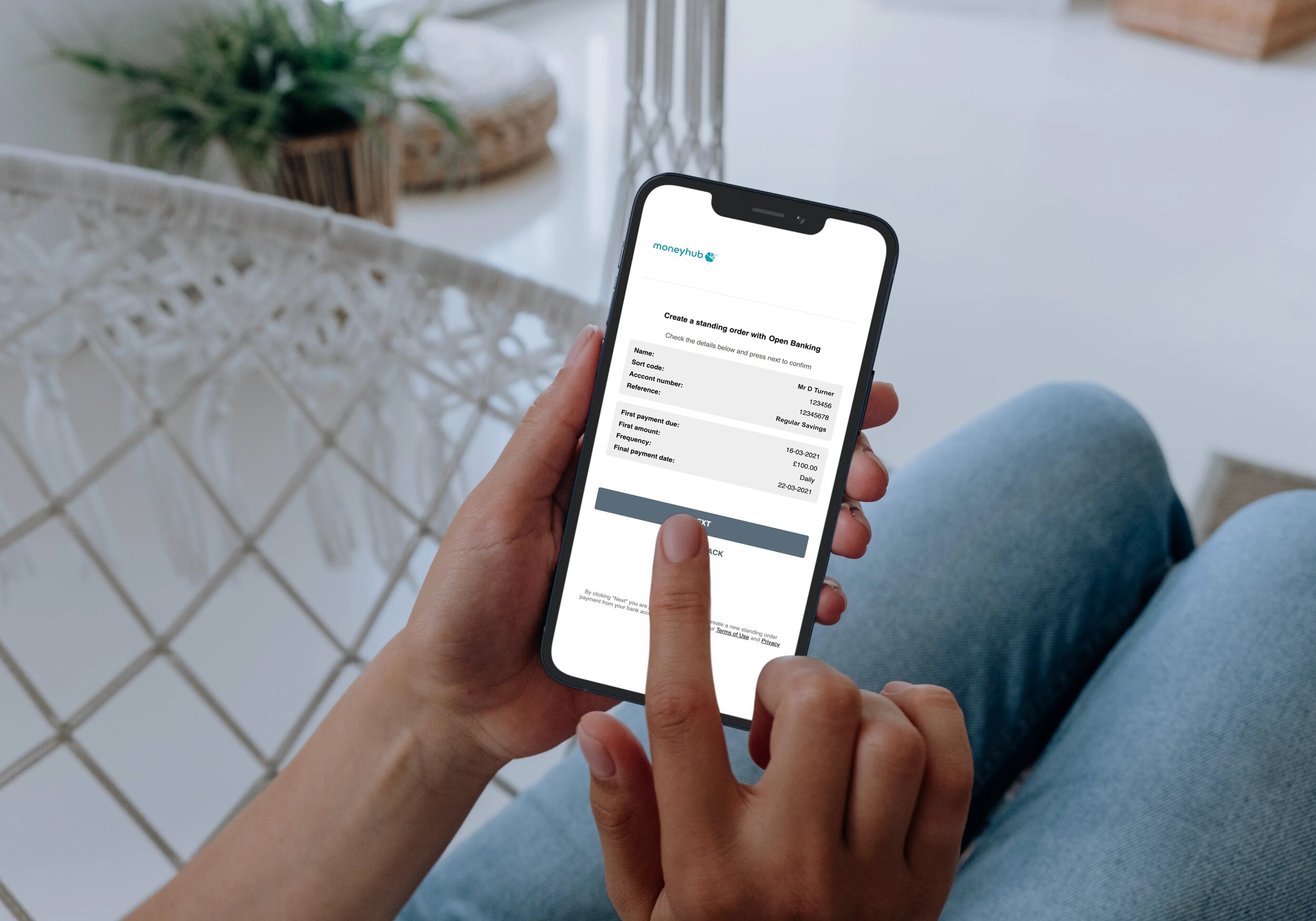

Standing orders have many use cases for your customers. They are the cheaper, faster and more secure way to make a Fixed Recurring Payment - and are just one of many features available through our Payment API.

Standing Orders are recurring scheduled payments for the same amount, with a frequency you choose, which are often used to pay for things such as rent, mortgage or any other fixed regular payment into savings, pensions or investment accounts. They can be executed to make automated payments either daily, weekly, monthly, or on another fixed schedule of your choice.

“Standing Orders are set up and controlled by the end user, giving consumers more visibility, and more control over making changes. ”

Using Open Banking payments, which allow a customer to transfer money from one bank account to another, Standing Orders are usually processed and received on the same day they are sent. As they are based on the same Faster Payments infrastructure used in current bank transfers, most Standing Order payments should be made almost immediately, if both accounts are part of the Faster Payments Scheme.

Standing Orders are set up and controlled by the end user, giving consumers more visibility, and more control over making changes.

Standing Orders are also a cheaper, faster and more secure way to make a Fixed Recurring Payment. There is no mandate to sign, no complicated guarantee to understand, and no card number to give away and be stored. Due to this, Standing Orders make a great alternative to ‘card on file’ or paying via Direct Debit. Direct Debits are set up by the end merchant, whereas Customers are also able to set a unique reference for each Standing Order to make it easy to reconcile the incoming payment when viewing their transactions.

“Standing orders can be set up to donate regularly to your chosen charity and these can be amended over time to change the amount of the donation and frequency at no cost to you or the charity. ”

A Standing Order is ideal for recurring account top-ups. The customer can ensure they are regularly added to a savings, investment or pension account that aligns to when they receive their salary each week or month. If a customer’s circumstances change - such as changing jobs or receiving a pay rise/cut - they can change the standing order instantly, without the fear of incurring any fees for cancelling or amending.

Standing Orders can be used to pay recurring household bills that are unlikely to change in cost each month - such as water, phone and broadband, or even rent or mortgage. For tenants living in a shared house, if one person pays a bill directly, Standing Orders from all tenants into the payer’s account for their portion of the payment can be a helpful way for customers to keep on top of who owes what.

The cost of setting up and using Standing Orders for regular payments is low, meaning a business can efficiently stay on top of their costs. Some small businesses also collect regular payments from customers by Standing Order knowing that payments will be collected automatically and on time.

Many people have subscriptions for magazines, food boxes, software or streaming services like Netflix or Amazon Prime, which charge a fixed fee on a monthly basis. A Standing Order can be the perfect option to pay these, as the Standing Order can be cancelled or modified by the user, rather than having to contact their bank to cancel a Direct Debit, for example.

Standing orders can be set up to donate regularly to a chosen charity and these can be amended over time to change the amount of the donation and frequency at no cost to the customer, or the charity. This is especially important in the post-Covid world, where 53% of charities reported a drop in donations since the start of the crisis (source: CAF UK Giving Three Month Coronavirus briefing).

Standing Orders are just one of many features you’ll receive as standard with our Payment API. Visit our Standing Order documentation to start building, or get in touch to find out more.

David is Moneyhub’s API, Payments and Connections Product Manager and is responsible for delivering new features for our API platform to enable fintechs and larger firms to build amazing customer experiences. He works with our existing clients to understand their needs so they can deliver more for their clients, and aims to continually improve our market fit to grow our customer base. David has over 10 years’ experience in Financial Services in project delivery, IT Operations and product ownership roles.In all his roles, David’s key focus has always been ensuring the technology solutions deliver fantastic and resilient outcomes.

To misquote Robert Burns, the best-laid plans of mice, men and financial service providers often go awry.

I firmly believe that everyone in the sector puts the best intentions of their customers first in the vast majority of cases. Do we always get it right? No. Companies are made of people, and people don’t always make the correct choices. Decisions made around Open Banking are no exception.

It is human nature to put off the non-essential. We prioritise urgency at the expense of practicality, often for the best reasons. Meetings are held to decide what is ‘business critical’ and the agenda items that don’t make the cut are mothballed. Sometimes, as in the case of API implementation by CMA9 banks, that means the customer's best interests are unintentionally sidelined.

That’s not a dig at CMA9 generally. The FCA required certain banks to make data available to third-party providers (TPPs) via standardised Open Banking APIs by September 2019 at the latest. Among other requirements, the regulator insisted banks align their API offerings for TPPs with their own customer offerings. It was a big piece of work and, given the complexity, the FCA granted a selective six-month extension to the deadline of September 2019 to the 14th March 2020 (only for those that did not have APIs live at that stage). At a stroke, the implementation – already two years in the planning – was put aside by stretched teams with other urgent projects on the planning board.

As well as introducing a delay, moving the goalposts suggested the deadline was something of a moveable feast. In showing leniency, the FCA may have inadvertently given the impression that the legal requirement was more of a serving suggestion than a clear instruction. Naturally, some banks took a slacker approach to API than was in their customers’ best interests. Many still have open tickets to be resolved at the moment with fluid deadlines for correction.

Some of the banks, of which the CMA9 are included, are relying on MCI (screen scraping) technologies instead of APIs despite the deadline and an extension to the deadline having now passed. In addition, TPPs like Moneyhub are having to adapt their own data infrastructure to accommodate customers whose banks have not satisfied the FCA requirement

Those banks have run their projects too close to the line and failed to deliver products that are fit for purpose.

One of the very best measures of efficacy in data sharing is ‘Time to Consent’, the number of seconds it takes to return a request for secure customer data. The speeds are averaged over a three-month period and use standard statistical analysis to iron out irregularities.

And there is good news for CMA9, some of which – such as Nationwide Building Society (42 seconds) – beat challenger bank Monzo (47 seconds). That’s not as good as the frontrunner, mobile-only challenger Starling Bank (18 seconds), but to be applauded nonetheless.

But without the concerted effort of all the major players in Open Banking, customers are being left with a substandard offering. At Moneyhub, we believe that Open Banking presents opportunities for everyone in the financial services sector to benefit from increased transparency. While Open Banking is designed to level the playing field between CMA9 and emerging banks, it presents opportunities for all that operate in Financial Services inclusive of the large banks.

Disruption has been good for big companies which embraced new technologies and devastating for those who failed to see the opportunities it presented. Open Banking is the sector’s opportunity to do what is best for its customers – increasing financial transparency, making it easier to switch when more appropriate products are available and ultimately enabling financial wellbeing.

Disruption has been good for big companies which embraced new technologies and devastating for those who failed to see the opportunities it presented. Open Banking is the sector’s opportunity to do what is best for its customers – increasing financial transparency, making it easier to switch when more appropriate products are available and ultimately enabling financial wellbeing.

It is possible to see how making customers’ data easily, quickly and securely available to other providers might not be in the best interests of established market leaders. Of course there are those suggesting CMA9 banks are deliberately dragging their heels to stymie competition from challenger banks. We feel, and indeed hope, that the reason for slow progress is more benign.

At Moneyhub, our view is that the legislative efforts of the regulator are not being taken seriously enough. Because the implementation of secure, fast APIs has been pushed down some banks’ list of priorities, customers are not being put first. HSBC (which services the popular John Lewis partnership card) will be using screen-scraping after missing the deadline, Lloyds similarly has not been able to meet the deadline when providing the St James’s Place cash account. This really isn’t good enough. Our industry is better than this.

Open Banking is the future of not just banking, but an array of financial services in a truly digital era. As I have said, it is human nature, and therefore business nature, to put non-urgent matters to one side. Yet, we live in a fast-moving world where putting customers first is paramount. Those who fail to get in line face a fate worse than the FCA’s anger; they will incur the wrath of their customers.

And we all know what happens then.

However, despite the increase in auto-enrolment rates and employer contributions rising to 5 per cent, there remains a significant gulf between what people are putting into their pension pots and the amount they will actually need to retire comfortably. A pensions crisis grips the nation; Britain’s ageing population and the rising costs of long-term elderly care is fast-creating a funding shortfall for sufficient support and the confusing pension tax relief system certainly hasn’t helped in incentivising Britons to save for the future.

If that wasn’t bad enough, new analysis of official data on UK household incomes indicates the gap between men and women’s pension income is more than twice that of the gender pay gap at 40%. According to a paper from the Centre for Policy Studies, 2018 was the year that saving in Britain dropped to a record low with households investing just 4.9% of their income for the future.

Experts suggest the reason behind the pensions gap (the difference between the current rate at which we are saving and the amount we will need for the future) stems predominantly from the complex nature of the pensions system. This is supported by findings from a study of UK workers conducted by PwC in which six in ten (59%) respondents said their lack of understanding puts them off saving more.

Unfortunately, solving the pensions crisis isn’t a simple case of increasing auto-enrolment rates. If workers today are to retire comfortably, government and industry must find a way to inspire people to take a proactive approach to their pensions. Fortunately, the introduction of PSD2 and the momentum towards open banking offers promise in the form of cutting-edge financial technology.

With seamless data sharing made possible through smart APIs, there is huge potential for banks to facilitate the act of future-proofing our finances through intuitive apps that make money management as quick and easy. Through open banking, there exists a real opportunity to provide customers with a holistic view of their finances across all accounts. With this in mind, pensions have the potential to become less of a dusty piggy bank on a bookshelf that no one wants to think about, to just another component of our unique financial profile that we top up every day.

Having recently been accepted into the Open Banking Implementation Entity regulatory sandbox, Moneyhub has an exciting opportunity to test innovative financial tech products, services and features that could be transformational for the consumer payment experience. Being able to do this within the sandbox, allows us to deploy to customer quickly, without the usual compliance hurdles that can stand in the way. We truly feel that tech has the potential to solve a whole raft of consumer finance problems, not least helping with our current pensions funding crisis. As such, a key part of what we will be trialling in the sandbox, is making managing finances easier with micro-payment using PISP (Payment Initiation Service Provider), with Starling Bank.

The idea is to create a system in which frictionless micro-payments are made to your pension pot with your consent, and integrated as part of your daily financial activity. Some of you may already be familiar with micropayments, but this is the first solution of its kind that automates micro-payments in real time to promote a proactive approach to saving.

Until now, any micro-payments a user intended to make would be tracked and compiled into one high transaction at the end of the month – a helpful feature, but it certainly doesn’t encourage better savings behaviour. Through our work with Starling Bank on micro-payments, Moneyhub will up your spare change in real-time - whether that’s 80p that you saved on your daily food budget or the £4 you saved on bus travel last Wednesday.

On the surface, it may not seem like much. However, a few pounds every day really adds up for retirement. Soon, the spare change that was swept up begins to make for a sizeable pile. As the interest accumulates, what started as a few pennies in a jar can quietly become a comfortable retirement income. Even just £2.50 a day for a 30 year old can grow to be worth £85k in retirement – a figure which seems daunting and out of reach today, but is perfectly achievable through daily micro-payments.

What’s more, I’m sure you’ll agree that it’s better to skim off a little extra from your daily spending and have it automatically sent to your savings than see a large lump sum leave your account at the same time your bills and rent are due. By taking advantage of the possibilities born from open banking, our goal is to encourage a shift in attitude. We want to help people to view forward-planning for their long-term finances not as an intimidating mountain to climb in the future but an achievable target that can be easily tackled through minimal daily contributions.

Already, our involvement with the sandbox has provided invaluable insight into consumer behaviour and revealed the positive impact that nudges can have on our saving and spending habits. We’ve found that it really doesn’t take much for people to start changing their financial behaviours – just a push in the right direction like a health tracking app encourages us to take more steps or drink more water.

Thanks to our integration of Starling Bank’s API into our payment gateway, users can already initiate a payment straight from one account to the other in real-time, whether it’s an ISA, a savings account or a pension pot. Our upcoming trial of micro-payments using PISP offers a new solution to tackling the pensions crisis. By embracing an open, API-led approach, banks can play a leading role in transforming the way people view their pensions.

Rather than a looming concern that becomes scarier the longer you put it off, planning for retirement can become a proactive measure that people find satisfying – and you would be surprised how much you could save. In the long-run, it’s the 20p spare you had on an idle Tuesday that could just make all the difference.

We’re living through an interesting period in financial services. From the revolution of open banking to the rapid rise of the robo-advisers, rarely has our industry seen so much disruption in such a short space of time.

For wealth managers, much of that innovation has focused on using algorithms to bring down costs and reach new audiences. The 130 (and counting) robo-advisers that have entered the market are a welcome addition, but is their potential being realised?

Underusing the algorithms

The problem isn’t with robo-products themselves – it’s with their scope.

Because the current crop of algorithmic advisers focus on only one aspect of users’ wealth, like their ISA or mortgage, they’re missing out on the opportunity to offer more holistic advice.

Open banking lets wealth managers take a much wider view of their customers’ finances and provide more suitable advice but few, if any, providers have yet to take full advantage of it and the market is due to see a surge of new players who will.

Let me give you an example.

Sarah wants to start investing. She’s been reading some articles online and thinks that a robo-adviser could be a cost-effective way to get started.

She’s not wrong. But what her ISA robo-adviser can’t see is that Sarah also has £5,000 of credit card debt and high-interest loan on her car.

Any human adviser would tell her that paying off her credit cards is a far more effective use of her savings. But with access to a very limited set of information, her robo-adviser can’t make that judgement call.

A better way

As any adviser will tell you, more information equals better advice.

Robo-advisers have the clear potential to offer truly holistic advice, but manual date entries and fact-finds fail are failing to unearth the required information. But by using open banking APIs to legally aggregate a customer’s date, the algorithms could access a much wider data set that includes credit cards, bank accounts and ISAs, and use it to generate suitable, targeted advice – while saving customers from spending hours on fact finding.

Providers could incentivise customers to add more APIs by giving them a reliability score. Adding one bank account would give you a lower score than if you also added your credit cards and ISAs, for example. It’s a smart way to encourage users to help wealth managers provide optimal financial advice.

Ultimately, we as an industry should always be looking for ways to improve the suitability of financial recommendations. Algorithms can go some way to facilitating this conversation – but surely gaining a better understanding of your customers’ date is the real answer, hidden in plain sight.

To find out how we can help your business evolve, get in touch on 0117 280 5155 or email enterprise@moneyhub.com.

It’s now been eight months since the Open Banking reforms were put in place. Designed to put the consumer back in control of their data, the top 9 banks (CMA9) had to provide an Open Banking connection (API) that regulated Third Party Providers (TPPs) with special permissions could connect to. This allows their customers to see all their finances in one place and use market leading tools to analyse their money.

Whether you want to create your own solution, or you want us to do it for you—we have the technology for it. Our experienced team is here to support you now and in the future.